The FTC has shut down Financial Education Services.

The FTC has shut down Financial Education Services.

Federal regulatory action against FES follows a $1 million pyramid scheme fine, issued by the state of Georgia in 2019.

As alleged by the FTC, FES “scamm(ed) consumers out of more than $213 million”.

Named defendants in the FTC’s Complaint are:

Named defendants in the FTC’s Complaint are:

- Financial Education Services INC. (Michigan)

- United Wealth Services INC. (Michigan)

- VR-Tech LLC (Michigan)

- VR-Tech MGT LLC (Michigan)

- CM Rent INC (Colorado)

- Youth Financial Literacy Foundation (Michigan)

- Parimal Naik (FES co-founder and CEO)

- Michael Toloff (FES co-founder and President)

- Christopher Toloff (FES co-founder) and

- Gerald Thompson (FES co-founder)

The marketing schtick behind Financial Education Services was credit repair.

Defendants claim they can successfully and permanently remove all negative information from consumers’ credit histories or credit reports.

Defendants also claim they will build a positive payment history for consumers by reporting their rental payments to credit reporting agencies, through their Credit My Rent service.

Defendants also claim they can obtain for consumers credit-building products, such as secured credit cards.

Defendants claim that these activities will significantly increase consumers’ credit scores and their eligibility for funding at lower interest rates.

BehindMLM reviewed FES in August 2018. The math behind commissions paid out didn’t make sense, nor did the service as a retail offering.

Retail is possible, however with affiliates forced to buy a service subscription to qualify for commissions, I’m not convinced it’s a focus.

Simply put: From a retail perspective Financial Education Services doesn’t make much sense.

An MLM company without a healthy retail offering lends itself to operating as a pyramid scheme.

The FTC has sued FES under the FTC and Telemarketing and Consumer Fraud and Abuse Prevention Acts.

Cited as a “credit repair scam”, here’s how the FTC describes FES in their Complaint;

Defendants falsely claim they can improve consumers’ credit scores by removing all negative items from their credit reports and adding credit building products.

In addition, Defendants market an investment opportunity—encouraging consumers to become FES Agents and then recruit other consumers to purchase Defendants’ credit repair services (often at the same time as marketing their credit repair services).

Defendants falsely claim that FES Agents will earn substantial income.

In reality, however, Defendants’ purported investment opportunity is an illegal pyramid scheme.

Defendants’ compensation plan incentivizes recruiting new FES Agents over selling credit repair services, and few consumers ever realize the promised earnings.

Looks like I was on the money.

On the marketing side of things, the FTC calls out FES’ website and use of “social media sites, such as Facebook, Instagram, and YouTube” to make “deceptive claims”.

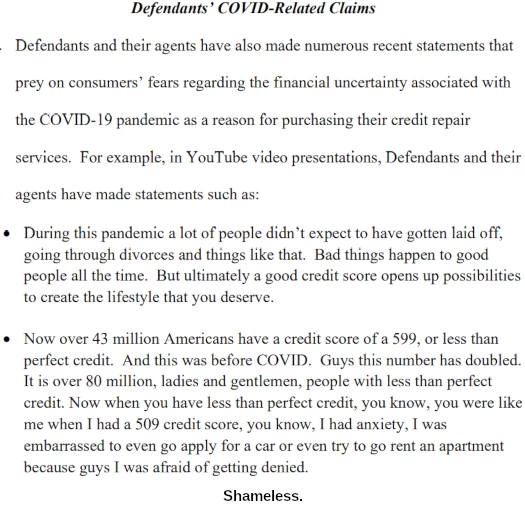

Multiple examples from FES and its promoters are cited, including predatory tactics exploiting COVID-19.

Telemarketing was also a big part of FES’ deceptive marketing campaigns;

When consumers then speak with Defendants’ representatives over the telephone, the representatives make many of the same deceptive representations included on Defendants’ websites and social media accounts.

Defendants’ representatives falsely claim that Defendants can remove negative items from consumers’ credit reports, including student loans, child support judgments, and bankruptcies.

Defendants’ representatives explain that they achieve their results by sending manual dispute letters to the credit reporting agencies.

Defendants’ representatives sometimes refer to their dispute process as something “the credit bureaus don’t want you to know about.”

Once Financial Education Services fees were collected, here’s what actually happened;

Defendants email consumers form dispute letters challenging, without support, all or almost all negative information in

consumers’ credit reports.Defendants instruct consumers to print the letters and mail them directly to the credit reporting agencies.

In numerous instances, however, these unsupported challenges have not caused credit reporting agencies to delete permanently or change the information.

Further, in many instances, the credit building products offered by Defendants do not have the positive impact on the consumer’s credit score promised by Defendants.

Some services provided by FES were completely pointless;

through their CreditMyRent brand, Defendants claim to report consumers’ positive rental history to TransUnion and Equifax.

Rental payments, however, do not factor in FICO® Score 8, the FICO score commonly used by lenders.

Not only did FES’ retail services make no sense from a pricing standpoint, they didn’t even provide the advertised service.

In short, in numerous instances, Defendants fail to remove negative information permanently from consumers’ credit reports. And in numerous instances, consumers who purchase Defendants’ credit repair services do not obtain the promised improvements to their credit scores.

Which, as predicted, saw FES primarily operate as a pyramid scheme.

Defendants also market a purported investment opportunity, soliciting consumers to become FES Agents to recruit additional consumers to purchase Defendants’ credit repair services and become FES Agents themselves.

This investment opportunity is, in reality, an illegal pyramid scheme.

Defendants claim that consumers who enroll as FES Agents will earn substantial income, typically in the form of commissions and bonuses, for the recruitment of new FES Agents and downstream revenue from the purchases by consumers of credit repair services.

When consumers speak with Defendants’ representatives regarding Defendants’ credit repair services, typically by telephone, the representatives often also try to recruit consumers to become FES Agents.

Defendants and their agents have also made numerous recent statements that prey on consumers’ fears regarding the COVID-19 pandemic and its financial effects as reason for enrolling in their investment opportunity.

In addition, Defendants’ representatives often emphasize the importance of recruiting new agents in communications with consumers.

Defendants’ trainings also focus more on, and emphasize, how to recruit new agents over selling credit repair services.

Many FES Agents, to remain FES Agents, continue to pay the monthly credit repair fee and many FES Agents are encouraged to pay, and do pay, registration fees for new FES Agents to improve their downline.

As a result, in many instances, FES Agents end up paying more money to Defendants than they receive from them.

In some instances, Defendants do not pay promised bonuses to FES Agents.

In the absence of significant retail sales, the FTC alleges Financial Education Services is a $467 million dollar pyramid scheme.

Defendants have collected at least $213,000,000 from consumers through their unlawful credit repair and investment opportunity scheme in the three years prior to the filing of this Complaint.

One additional particularly objectionable aspect of FES I’ll add was the use of a registered non-profit to further their scam.

Youth Financial Literacy Foundation (“Youth Financial”) is a Michigan nonprofit corporation

Youth Financial was originally incorporated as MSU Common Sense, Inc., which changed its name to The Thompson Scholarship Foundation, Inc., which changed its name to Patro Scholarship Foundation, Inc., which changed its name to Youth Financial.

Youth Financial has also done business as American Credit Education Services, Financial Education, Financial Literacy Education Services, and United Credit Education Services.

At all times relevant to this Complaint, Youth Financial has carried on business for its own profit or that of its members.

If for nothing else, I really think that speaks to the character of FES’s co-founders.

Specific counts of fraud in violation of the FTC Act include:

- misrepresentations regarding credit repair services;

- illegal pyramid;

- misrepresentations regarding investment opportunities;

- means and instrumentalities;

- violation of prohibition against charging advanced fees for credit repair services;

- failure to make required disclosures;

- failure to obtain signed contracts from consumers;

- failure to include required terms and conditions in contracts;

- failure to provide cancellation form;

- failure to provide consumers with copy of contract and other disclosures; and

- use of remotely created checks

The FTC also contends FES’ pyramid scheme violates the Credit Repair Organizations and Telemarketing Sales Rule Acts.

The FTC is seeking a permanent injunction and monetary relief against FES.

The FTC’s Complaint was filed under seal in the Eastern District of Michigan on May 23rd. An ex-parte Motion for a Temporary Restraining Order accompanied the Complaint.

On May 24th the Court granted the requested restraining order.

Defendants operated and promoted a marketing scheme in which they appear to have:

a. operating an illegal pyramid scheme;

b. in numerous instances, falsely representing that consumers who become agents (“FES Agents”) to recruit new FES Agents will earn substantial income; and

c. providing the means and instrumentalities for the commission of deceptive acts and practices by furnishing consumers with promotional materials to be used in marketing credit repair services and recruiting new FES Agents.

There is good cause to believe that Defendants have taken in gross revenues of approximately $467 million as a result of their unlawful practices.

There is good cause to believe that immediate and irreparable harm will result from Defendants’ ongoing violations of the FTC Act.

The granted TRO, among other things, freezes the FES Defendant’s assets. In a win for victims of FES’ pyramid scheme, a Temporary Receiver has also been appointed.

Looking forward, a preliminary injunction hearing has been scheduled for June 6th.

If the FTC prevails, both the TRO and Receivership will be made permanent.

Please be advised that it is far too early to discuss potential recovery. We’ll know more once the Receiver files their first report but there’s no timeline for that.

And that is of course assuming the FTC prevail on June 6th. Stay tuned.

Update 7th June 2022 – On June 1st the parties jointly requested the preliminary injunction hearing be continued.

The parties seek a continuance until the week of June 20, 2022, of the preliminary injunction hearing currently scheduled for Friday, June 3, 2022.

No reason for the requested extension was provided.

The court approved the joint motion on June 2nd. The preliminary injunction hearing has been rescheduled for June 30th.

The granted TRO remains in place till then.

Update 9th July 2022 – As per a Minute Entry order for virtual proceedings held on July 8th;

Judge instructed parties to submit one proposed order or individual proposed orders if there is no agreement to unfreeze bank accounts by 7/11/2022.

The Court will review all proposed order(s) and will issue its final order(s) by 7/13/2022.

There is still no preliminary injunction order following the hearing on June 30th. I’m assuming that will be addressed by the 13th July deadline the court has given itself.

Update 29th July 2022 – The FTC’s motion for a preliminary injunction against FES has been denied. At time of this update we still don’t know why.